The Global Meat Alternatives Market is analyzed in this report across source, product, shelf life, distribution channel, and region, highlighting major trends and growth forecasts for each segment.

Introduction:

Meat alternatives—also known as meat substitutes, analogs, or plant-based meats—are food products designed to replicate the taste, texture, appearance, and nutritional profile of conventional animal meat, using non-animal sources. As consumers, manufacturers, and policymakers increasingly prioritize sustainability and health, the global meat alternatives market is undergoing a major transformation. These products are emerging as a scalable solution to the ethical, environmental, and health-related concerns tied to traditional meat production. Typically made from plant proteins, fungi, microbial fermentation, or cultured cells, meat alternatives are being integrated into a wide range of applications, including burgers, sausages, nuggets, deli slices, and seafood analogs across retail, foodservice, and institutional channels.

Driven by rising climate concerns, animal welfare awareness, and the growing popularity of flexitarian and plant-forward lifestyles, the global market is on a steep growth trajectory. It is projected to reach USD 31.64 billion by 2030. This expansion is also supported by the increasing incidence of lifestyle-related diseases, growing interest in food sustainability, and rapid innovation in food technologies. The market was valued at approximately USD 10.6 billion in 2024 and is forecast to grow at a CAGR of 22.36% over the forecast period.

Market Dynamics:

The meat alternatives market is advancing rapidly, shaped by shifting consumer behavior, environmental imperatives, and technological breakthroughs.

Key market drivers include growing awareness of the environmental footprint of livestock production, rising health consciousness, and accelerating adoption of flexitarian diets. Sustainability concerns—such as greenhouse gas emissions, deforestation, and water consumption—are pushing consumers and governments toward more eco-friendly food systems. Health-related motivations are also central, with consumers seeking alternatives to red and processed meat in response to risks of heart disease and high cholesterol. A 2021 World Health Organization (WHO) report emphasized the public health benefits of reducing red meat intake, reinforcing demand for alternative proteins. In parallel, data from The Vegan Society indicated that over one-third of UK consumers reduced their meat consumption in 2021, and 20% cut back on dairy—clear indicators of evolving dietary norms.

Technological innovation continues to accelerate adoption. Advances in high-moisture extrusion, precision fermentation, and ingredient engineering have significantly improved the sensory and nutritional attributes of meat analogs. These enhancements are making alternative proteins more appealing and accessible to mainstream consumers.

The market offers considerable growth potential across multiple vectors. Opportunities include expansion in retail and foodservice plant-based offerings, rising investment in fermentation and cultivated meat technologies, and the development of culturally attuned products for emerging markets. Companies are leveraging biotechnology, flavor science, and novel proteins like mycoprotein to diversify product portfolios. Hybrid products—combining plant-based and cultivated elements—are also gaining traction as scalable, functional formats. In a strong show of institutional backing, the European Investment Bank (EIB) committed €20 million in venture debt financing to Matr Foods in September, supporting fermentation-based meat alternative production as part of the EU’s broader food-tech agenda.

Emerging trends are further shaping the industry. These include the rise of fungi-based whole-cut alternatives, the use of AI in ingredient formulation and sensory profiling, and heightened consumer preference for clean-label, minimally processed, allergen-free, and protein-rich products. Regulatory frameworks are also evolving to support clearer labeling and public investment in alternative protein R&D. As product innovation continues and capacity scales, meat alternatives are rapidly shifting from a niche offering to a core component of future-ready, sustainable food systems.

Segment Highlights and Performance:

By Source:

Plant-based alternatives lead the source segment, accounting for approximately 65% to 70% of the global market. Their dominance stems from widespread availability of plant proteins—such as soy, wheat, and pea—along with strong consumer familiarity, mature product development, and broad retail and foodservice penetration. Demand for sustainable, clean-label, and allergen-conscious products continues to fuel growth in this segment.

By Product Type:

Burger patties are the top-performing product category, holding 32% to 35% of the market. Their mainstream appeal, convenience, and compatibility with fast-food and home-cooked formats make them the most recognized face of the meat alternatives category. Flagship products like the Beyond Burger and Impossible Burger have helped drive category visibility and trial.

By Shelf Life:

Frozen products dominate the shelf life segment with 39% to 55% of the market. Their longer shelf life, reduced need for preservatives, and storage efficiency have made frozen alternatives a staple in global supermarket chains. Strong cold-chain infrastructure and rising demand for ready-to-cook plant-based meals further bolster this segment.

By Distribution Channel:

Retail distribution is the largest channel, accounting for 49% to 63% of global sales. Supermarkets and hypermarkets offer high product visibility, competitive pricing, and convenient access, supported by dedicated plant-based sections and private-label brand expansion. Major chains like Tesco, Walmart, and Carrefour are playing a key role in normalizing meat alternatives on retail shelves.

Geographical Analysis:

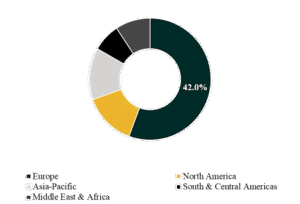

The global meat alternatives market is segmented across North America, Europe, Asia-Pacific, South & Central America, and the Middle East & Africa.

Europe holds the largest regional share, contributing approximately 42% of global market value. The region’s strong alignment with sustainability, animal welfare, and clean-label preferences—coupled with supportive regulatory frameworks—has made it a global leader. European consumers have increasingly embraced flexitarian diets, while retailers and foodservice operators have significantly expanded plant-based offerings.

Asia-Pacific is forecast to post the highest CAGR in the global meat alternatives market. Key growth drivers include rising health awareness, increasing disposable income, and demand for scalable protein solutions across densely populated countries like China, India, and Japan. Cultural familiarity with plant-based ingredients, combined with robust investment in food-tech startups and infrastructure, is accelerating adoption across the region.

The global meat alternatives market features a competitive mix of legacy food companies, emerging startups, and specialized protein innovators. Companies are competing on innovation, ingredient transparency, and market access—often through partnerships with major retailers and foodservice providers.

Notable players include Beyond Meat, Impossible Foods, Kellogg Company, Maple Leaf Foods, Nestlé, Unilever, Tyson Foods, JBS, Hormel Foods, and Believer Meats. These companies are advancing differentiated product lines, scaling production, and expanding geographically to capitalize on shifting consumer preferences and regulatory momentum.

Segmentation:

By Source:

By Product:

By Shelf Life:

By Distribution Channel:

Companies included in the report: