The Global AI Assistants Market is analyzed in this report across types, deployment modes, end-use industries, and regions, highlighting major trends and growth forecasts for each segment.

Introduction:

Artificial Intelligence (AI) assistants are fundamentally reshaping how individuals and organizations interact with technology. These intelligent systems are embedded across a wide spectrum of applications, from personal voice assistants in smartphones and smart homes to enterprise-grade conversational agents that streamline business processes and elevate customer experiences.

The global AI assistants market is undergoing exponential growth, projected to reach USD 64.30 billion by 2030. This surge is driven by increasing automation needs, growing digital fluency, and rising consumer preference for real-time, personalized interactions via voice and text. The integration of generative AI, rapid enterprise adoption, and demand for always-on support are accelerating market momentum. Valued at approximately USD 5.83 billion in 2024, the market is set to expand at a CAGR of 46% over the forecast period.

The AI assistants market is advancing at a transformative pace, fueled by the convergence of automation demand, user behavior shifts, and breakthroughs in natural language processing (NLP), machine learning, and generative AI. These assistants are revolutionizing workflows by automating repetitive tasks, providing real-time insights, and enhancing service interactions across sectors.

Cloud infrastructure and open APIs have lowered barriers to deployment, enabling scalable rollout of AI assistants across industries and user bases. From healthcare and finance to education and retail, organizations are leveraging AI assistants to improve efficiency, responsiveness, and operational resilience.

Government-backed AI strategies are further accelerating market development. The U.S. national AI strategy emphasizes trustworthy, human-centric AI deployment, while India’s recently launched IndiaAI Mission promotes a full-stack ecosystem for innovation, talent development, and research. These initiatives are catalyzing public-private investments and enhancing global competitiveness in AI assistant technologies.

Significant growth opportunities lie in the deployment of enterprise assistants for IT support, HR automation, customer service, and sales enablement. As voice and multimodal AI assistants expand into automotive, smart home, and wearable tech ecosystems, new consumer touchpoints are opening across industries. Emerging agentic AI systems, capable of autonomous, multi-step decision-making, are redefining productivity by supporting complex workflows such as content generation, research, and data analysis.

Key trends shaping the market include the evolution of generative and emotionally intelligent assistants, growing demand for AI co-pilots in knowledge work, and heightened focus on AI ethics, privacy, and explainability. Generative AI is enabling assistants to synthesize content, reason dynamically, and adapt fluidly to user intent. Enterprises are increasingly turning to customizable, privacy-respecting models that deliver intelligent automation while maintaining data control.

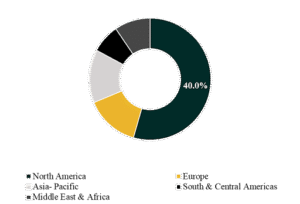

The global AI assistants market is examined across key regions, including North America, Europe, Asia-Pacific, South & Central America, and the Middle East & Africa.

North America leads the global AI assistants market with a 40% share, underpinned by robust digital infrastructure, strong enterprise adoption, and the presence of leading AI technology firms. Early investments in cloud computing, NLP, and conversational AI platforms have positioned the region at the forefront of innovation and deployment.

Asia-Pacific is expected to record the highest compound annual growth rate, ranging between 16% and 31%. This growth is fueled by rapid digitalization, government-backed AI programs, and mass adoption of smartphones and smart assistants in countries like China, India, and Japan. The region’s thriving tech ecosystem and consumer openness to voice and generative AI solutions are propelling it into a leadership position in global AI assistant adoption.

The competitive landscape is shaped by a mix of global technology leaders, enterprise software firms, and fast-scaling AI startups. Companies are differentiating through large-scale language model integration, vertical-specific assistant platforms, and seamless ecosystem partnerships.

Key players profiled in this report include: Google, Apple, Microsoft, Amazon, Meta, Salesforce, SAP, Zoom, SoundHound AI, and LivePerson.

These firms are investing heavily in generative AI, real-time agentic systems, and domain-specific assistants, competing to redefine the future of AI-powered interaction across enterprise and consumer markets.

Segmentation:

By Type:

By Deployment Mode:

By End-User Industry:

Companies included in the report: