The Global Premium Packaged Food Market is analyzed in this report across product type, distribution channel, and region, highlighting major trends and growth forecasts for each segment.

The global premium packaged food market is experiencing steady growth, driven by rising consumer demand for high-quality, convenient, and indulgent food experiences. This market segment addresses evolving dietary preferences, heightened health awareness, and a growing appetite for gourmet offerings. Key categories include dairy and dairy alternatives, snacks and savory products, bakery and confectionery, ready-to-eat meals, and beverages.

This upward trend is fueled by increasing disposable incomes, urbanization, and a shift toward healthier, more convenient food choices. In 2024, the market was valued at approximately USD 264 billion and is projected to reach USD 376.6 billion by 2030, growing at a CAGR of 6.1% over the forecast period.

Several factors are shaping the growth trajectory of the global premium packaged food industry. Core drivers include rising demand for quality-driven and convenient food products, increasing health and wellness consciousness, and a growing middle- to high-income consumer base in urban areas. In response, manufacturers are investing in clean-label formulations, functional and fortified offerings, and premium ingredients to differentiate their portfolios and build brand loyalty.

Operational improvements across packaging, distribution, and supply chain logistics have supported broader access to premium foods, ensuring freshness and enhancing the overall consumer experience. Retail innovation and omnichannel availability are also enabling faster product adoption across both developed and emerging markets.

The market presents compelling growth opportunities. Areas of expansion include the launch of premium ready-to-eat and ready-to-cook meals, a surge in plant-based and functional foods, and direct-to-consumer strategies to reach niche segments. Brands are tailoring offerings to target affluent households, health-focused individuals, and urban professionals—aligning with lifestyle preferences and dietary demands. Compliance with regulatory frameworks such as the FDA’s “healthy” labeling guidance and India’s FSSAI packaging standards also reinforces consumer trust and brand credibility.

Notable trends redefining the market include rising interest in organic and natural products, increased demand for functional nutrition, and the use of eco-conscious packaging. As sustainability becomes a competitive differentiator, brands are shifting toward ethically sourced ingredients and recyclable materials. Simultaneously, the growth of e-commerce and subscription-based food services is allowing companies to personalize offerings, build direct relationships with consumers, and deliver curated premium experiences.

By Product Type

Bakery & Confectionery products lead the premium packaged food category, capturing approximately 30% to 35% of market share. This segment benefits from strong consumer interest in artisanal bread, premium chocolates, and indulgent baked goods—driven by their blend of quality, flavor, and convenience. These products are closely associated with gifting, everyday indulgence, and lifestyle consumption, making them especially popular among urban and affluent demographics.

By Distribution Channel

Supermarkets and hypermarkets are the primary distribution channels for premium packaged foods, contributing roughly 40% to 45% of global sales. These outlets offer a broad assortment of premium SKUs under one roof, enabling consumers to explore, compare, and discover new products easily. Strong in-store visibility, strategic product placement, and promotional activity further reinforce their position as the leading retail channel.

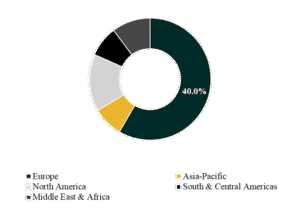

The global premium packaged food market is analyzed across North America, Europe, Asia-Pacific, South & Central America, and the Middle East & Africa.

Europe leads the market, accounting for approximately 40% of global share. This dominance is supported by mature retail infrastructure, high consumer preference for quality and organic foods, and a strong base of established premium brands.

In contrast, Asia-Pacific is expected to post the fastest growth, with a projected CAGR of 7% to 8%. This growth is driven by rising incomes, rapid urbanization, and increasing consumer demand for premium, convenient food options in dynamic markets such as China, India, and Japan.

The premium packaged food market is marked by the presence of global food corporations, regional players, and specialty brands—all competing through innovation, premium sourcing, and diversified distribution strategies.

Leading market participants include Nestlé S.A., Mondelez International, General Mills Inc., Kraft Heinz Company, Mars, Incorporated, Unilever N.V., Tyson Foods, Inc., Cargill, Incorporated, Lindt & Sprüngli, Ferrero Group, Barilla Group, Premier Foods, and Smithfield Foods. These companies continue to invest in product innovation, brand elevation, and strategic retail partnerships to strengthen their foothold in the high-margin premium segment.

Segmentation:

By Product Type:

By Distribution Channel:

Companies included in the report: